The landscape of private Medicare has just undergone its most significant regulatory transformation in years. In a sweeping final rule released in early April 2026, the Centers for Medicare & Medicaid Services (CMS) officially locked in a massive overhaul of the Medicare Advantage (MA) Star Ratings system.

While the new rules promise to funnel billions of dollars back into the pockets of high-performing insurers, CMS made a controversial U-turn on a proposed consumer protection: a mid-year “special enrollment window” that would have allowed seniors to ditch their plans if their favorite doctors were kicked out of the network.

From the removal of “administrative noise” to the delay of major health equity incentives, here is the definitive guide to what the 2026–2027 Medicare Advantage changes mean for insurers, providers, and the 34 million Americans enrolled in these plans.

The $18.6 Billion Pivot: Re-Engineering the Star Ratings

The Star Ratings system is the heartbeat of Medicare Advantage. It’s a 1-to-5 scale that determines which insurance companies receive Quality Bonus Payments (QBPs)—a pool of money that reached over $12 billion annually in previous years.

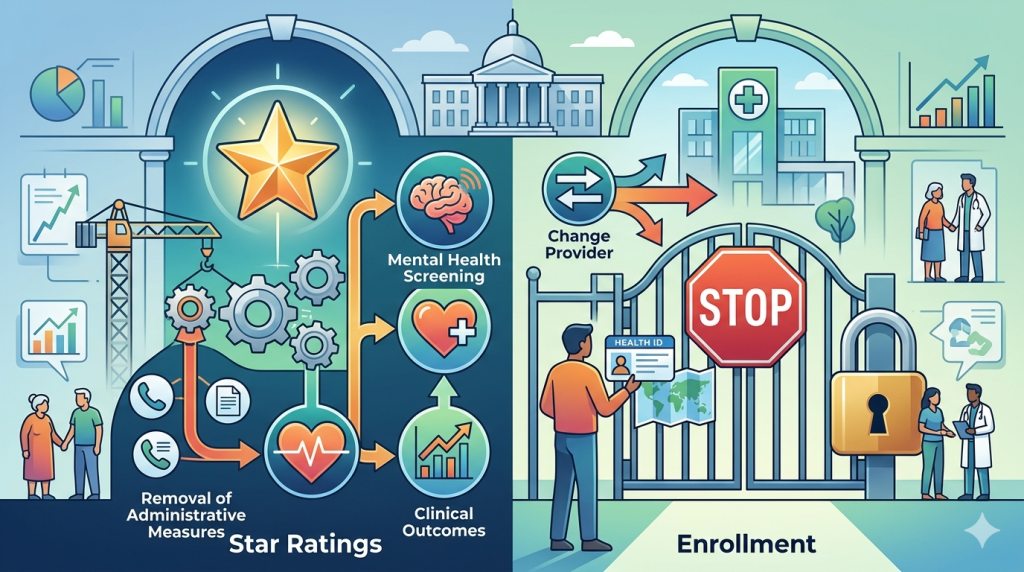

1. Slashing 11 “Process” Measures

For years, insurers argued that the Star Ratings were cluttered with “easy” metrics that didn’t reflect true health outcomes—things like how quickly a call center agent answered the phone.

The Change: CMS has finalized the removal of 11 Star Ratings measures. These were largely administrative metrics where almost all plans performed at a high level, making it impossible for beneficiaries to distinguish between a “good” plan and a “great” one.

The Impact: By removing these low-variation measures, CMS is statistically making it easier for many plans to achieve or maintain 4-star status. This is projected to cost the Medicare Trust Fund $18.6 billion over the next decade in increased bonus payouts.

2. Outcomes Over Administration

With the removal of administrative fluff, the remaining metrics—focused on clinical outcomes (like blood sugar control and cancer screenings)—now carry significantly more weight. Clinical performance is expected to jump from representing 50% of a plan’s total score to nearly 65% by 2027.

3. The Behavioral Health Mandate

In a move to address the nation’s mental health crisis, CMS added a new Depression Screening and Follow-Up measure. Starting with the 2027 measurement year (impacting 2029 ratings), insurers will be held financially accountable not just for screening seniors for depression, but for proving they provided actual follow-up care within 30 days of a positive screen.

The Enrollment U-Turn: Why You Can’t “Follow Your Doctor” (Yet)

The most debated part of the 2026-2027 proposal was a new Special Enrollment Period (SEP). This would have allowed a beneficiary to switch plans mid-year if their primary care doctor or a major hospital system left their plan’s network.

The Industry Pushback

Insurance giants lobbied fiercely against this rule, arguing that allowing patients to leave whenever a contract dispute occurred would destabilize the market and make it impossible to price plans accurately.

The CMS Decision

In the final rule, CMS chose not to implement this enrollment window. Instead of a permanent right to switch, the agency stated it needs more time to “consider the broad interest and complex feedback.”

Current Reality: If your doctor leaves your network in June, you are generally stuck with that plan until the next Open Enrollment period in October—unless you can prove the plan’s online directory was intentionally misleading.

The Health Equity “Freeze”

In another surprise move, CMS decided not to move forward with the “Excellent Health Outcomes for All” reward (formerly known as the Health Equity Index).

This index was designed to reward plans that showed exceptional care for socially vulnerable populations (such as those on dual-eligible Medicaid or low-income subsidies). Instead, CMS will stick with its “historical reward factor” while it re-evaluates how to incentivize equity without creating unintended financial imbalances.

Winners and Losers: The 2026 Performance Map

The release of the 2026 Star Ratings data alongside this rule shows a market in flux.

| Insurer | 2026 Star Performance | Market Outlook |

| UnitedHealthcare | Stable | Maintained a high percentage of members in 4+ star plans; continues to dominate the bonus pool. |

| Centene & Elevance | Gained Ground | Both saw significant recoveries in their ratings, reclaiming hundreds of millions in potential bonuses. |

| Humana | Struggling | A shock to the system: Humana reported that less than 25% of its members are in 4-star plans for 2026, down from nearly 90% previously. |

| Aetna (CVS Health) | Mixed | Saw a moderate decline in 4-star membership, though still remains a top-tier competitor. |

What This Means for the Average Senior

While most of these changes happen “under the hood,” they will eventually hit your mailbox and your wallet:

More Stable Benefits: Because CMS is making it slightly easier to get bonuses (by removing the 11 administrative measures), your plan is less likely to cut dental or vision “extras” in 2027.

Increased Out-of-Pocket Caps: The rule codifies the $2,000 out-of-pocket cap on prescription drugs (Part D) established by the Inflation Reduction Act, ensuring no senior pays more than that for meds starting in 2025/2026.

Strict Marketing Rules: CMS is cracking down on “Third-Party Marketing Organizations.” You should see fewer “Joe Namath style” TV commercials promising $0 premiums that don’t actually apply to your zip code.

Conclusion

The 2027 Final Rule is a masterclass in regulatory compromise. By providing an $18 billion “olive branch” to insurers through streamlined Star Ratings, CMS is attempting to stabilize a market that has been rocked by rising healthcare costs. However, by failing to finalize the provider-termination enrollment window, the agency has sent a clear message: Market stability takes precedence over beneficiary mobility—for now.

As clinical outcomes become the “new gold standard,” insurers that focus on actual medicine rather than administrative paperwork will be the ones that survive the 2027 transition.

Frequently Asked Questions (FAQ)

1. Can I switch my Medicare Advantage plan if my doctor leaves the network mid-year?

No. CMS did not finalize the proposed rule that would have allowed this. You must typically wait for the Annual Enrollment Period (Oct 15 – Dec 7) to switch. The only exception is if you can prove your plan provided “materially inaccurate” information about their network.

2. Why did CMS remove 11 Star Rating measures?

CMS found that almost every plan was getting a perfect score on these administrative tasks. Because there was no difference in performance, these metrics weren’t helping seniors choose better plans—they were just “inflating” scores.

3. What is the new “Depression Screening” requirement?

Starting in 2027, your Medicare Advantage plan will be graded on whether it successfully screens you for depression and—more importantly—whether it helps you find treatment if you need it. This makes mental health a top-tier financial priority for insurers.

4. Will my monthly premiums go up because of these changes?

Likely not. In fact, because the Star Rating overhaul is expected to result in more bonus money being paid to insurers, many plans may use that extra cash to keep premiums at $0 to remain competitive.